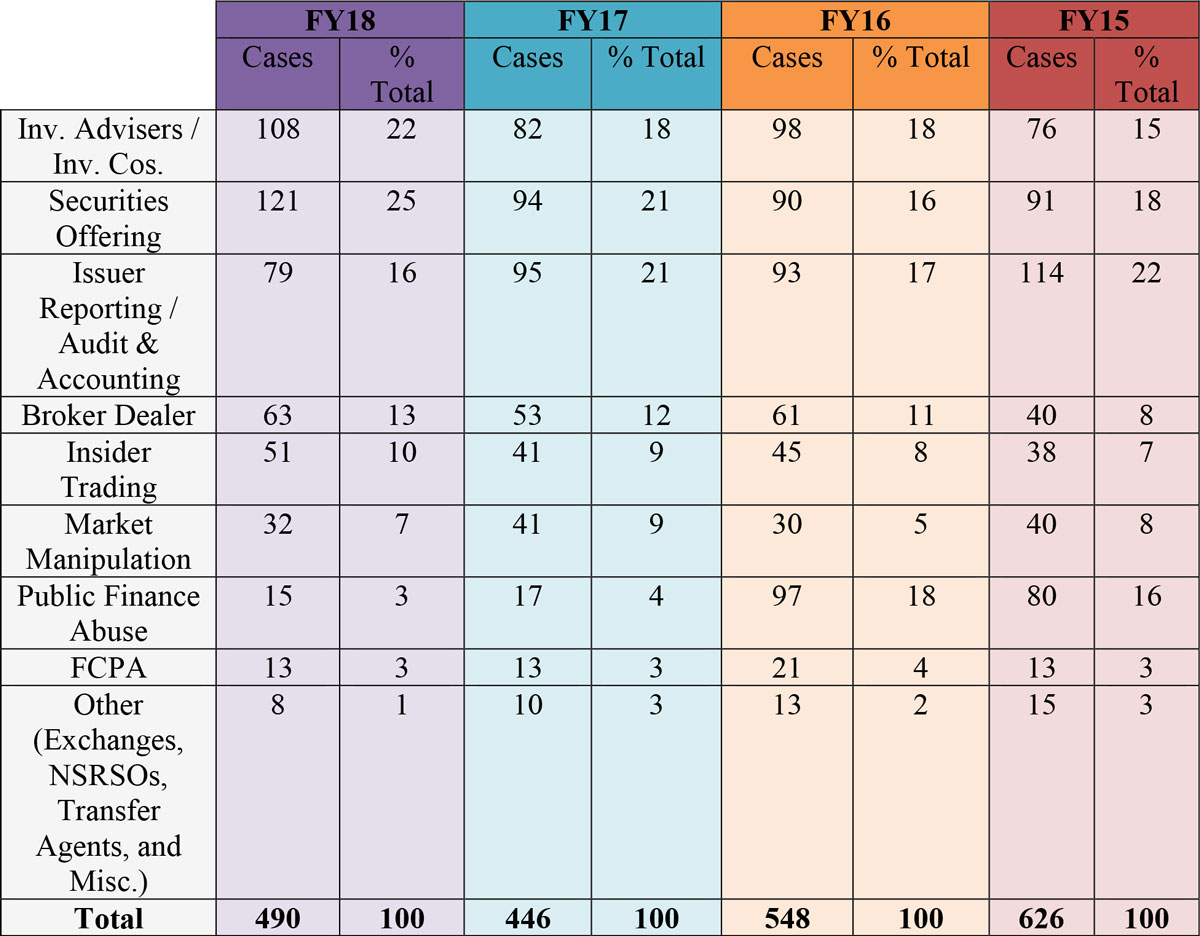

Due to a flurry of enforcement activity in the last quarter of Fiscal Year 2018, which closed at the end of September, the Securities and Exchange Commission filed nearly 10% more cases in 2018 than in the year before. The agency topped last year's numbers in every major category of cases except issuer disclosure and accounting, which were down about 13% from 2017.[1] Consistent with public statements made by Jay Clayton when he assumed the role of SEC Chairman in May 2017, the Commission focused its enforcement activity on "retail fraud," bringing 38% more cases involving securities offering frauds. However, enforcement in several other program areas was up as well. Actions against investment advisers were up nearly 38%, and those against broker-dealers were up 17%. Insider trading cases increased by approximately 24%.

Although the Commission entered its third quarter with enforcement actions down more than 15% from 2017—leading some commentators to speculate that enforcement would decline overall—the agency managed to catch up in the final three months, bringing 490 standalone actions in 2018 compared to 446 in 2017. Indeed, it appears that the SEC brought around 47% of all 2018 cases in the last quarter. When combined with actions to deregister public companies that were delinquent in their SEC filings ("12(j) proceedings") and administrative proceedings seeking bars based on the outcome of Commission actions or actions by criminal authorities or other regulators ("follow-on proceedings"), the Commission filed 821 total enforcement actions as compared to 754 actions last year—a surprising increase of 9%, considering the agency's slow start. That result comes with an important caveat: although the number of cases the SEC brought has increased, by one measure, the money recovered from cases brought in 2018 has declined about 42% compared to cases brought in 2017.

The Division of Enforcement's Co-Directors, Stephanie Avakian and Steven Peikin announced their goals for this year in the Division's 2017 Annual Report, issued last November. The 2017 Report set out several "core principles" of the SEC's enforcement agenda. These included focusing on the "Main Street investor"; seeking individual accountability; keeping pace with technological change; imposing sanctions that advance the Division's enforcement goals; and constantly assessing the allocation of the Division's resources. In this year's Report, the Co-Directors concluded that their results demonstrate a "faithful adherence to those principles."[2]

In our view, the Division clearly has advanced some of its core principles, though perhaps at a cost to other traditional enforcement priorities.

I. 2018 Enforcement Results by Case Category

The SEC has operated under a hiring freeze for nearly two years. As the Division of Enforcement shrinks, its decisions on how to deploy personnel across an expansive program become harder each year. According to the 2018 Annual Report, including contractors, the Division's total headcount is down about 10% from its peak in 2016.[3] Chairman Clayton noted in congressional testimony requesting a budget increase for 2019 that hiring certain additional personnel will be necessary "to effectively carry out [the SEC's] core mission," and, specifically, the Commission requested 17 additional enforcement personnel in its 2019 budget justification. Thus far, Congress appears amenable to that request, with both the House and the Senate separately adopting Fiscal Year 2019 appropriations legislation that funds the SEC's request. However, at least for now, the Commission continues to operate under stopgap measures at continuing Fiscal Year 2018 levels.

Budget negotiations aside, given the increase in cases, the Division argues in its 2018 Report that it has managed to do more with less.[4] Still, the Division also acknowledged that "additional resources would support two key priorities of the Division: protecting retail investors and combating cyber-related threats."[5] And as senior SEC officers will tell you, the numbers tell only part of the story. In some key areas, the mix of cases the Division brought in 2018 is significantly different than in prior years. Thus, it remains unclear to us whether the Division is doing more with less, or has just shifted its priorities to matters that take less time to complete.

A. Areas of Emphasis

The increase in offering fraud and investment adviser cases and concurrent decline in corporate accounting and disclosure matters in 2018 is seemingly consistent with the Division's stated priority to focus on retail investors. The 2018 Report rejects the notion that there is "a binary choice between protecting Main Street and policing Wall Street."[6] Nevertheless, enforcement resources have declined, making such a trade-off hard to avoid. And the shift from time-intensive accounting cases to "penny stock" and other offering frauds suggests that some sort of trade-off likely occurred.

Shifts in the SEC's exam program also could explain the 38% increase in investment adviser cases in 2018. The misconduct alleged in those cases ran the gamut from alleged misappropriation to misrepresentations to undisclosed conflicts of interest and other breaches of fiduciary duty. Noting that "[t]he number of registered advisers, their complexity, and their assets under management has increased substantially over the last decade," Peter Driscoll, Director of the SEC’s Office of Compliance Inspections and Examinations ("OCIE"), reported last year that between 2015 and 2016, OCIE increased the number of inspections by more than 20%, with more than half of those focused on investment advisers. He also reported an OCIE staff increase of 20% in 2016, which likely increased exam referrals to the Division of Enforcement in 2017 and 2018. In fact, in its full-agency 2017 Annual Report, the SEC noted that its examination coverage of investment advisers nearly doubled over the past five years from 8% to 15%.[7] And in this year's Enforcement Division Report, the Division highlighted its new "Share Class Selection Disclosure Initiative," examining "misconduct that occurs in the interactions between investment professionals and retail investors," with a particular focus on so-called "12b-1 fees" charged by investment advisers in the mutual fund industry.[8] Likely reacting to the increasing number of these cases and the two years on average that it takes to investigate them, the Division established an ongoing voluntary-disclosure initiative, permitting participating advisers to avoid penalties in exchange for quick settlements involving antifraud charges and disgorgement. We expect that this initiative will cause a significant increase in the number of investment adviser cases brought next year.

Notwithstanding a significant decrease in SEC broker-dealer exams due to the reorganization of OCIE a few years ago, the SEC has managed to keep the number of enforcement actions against broker-dealers consistent, or even increasing, year-over-year. Those cases were 13% of the SEC's total 2018 enforcement caseload versus 12% in 2017, 11% in 2016, and just 8% in 2015. And, according to case data compiled by the New York Times, along with this uptick in broker-dealer cases came an uptick in their associated recoveries. Whereas the Division recovered about $190 million for its 53 2017-filed broker-dealer cases, we calculate that it recovered about $209 million this past year for its 63 cases—an increase of about 9%.[9]

B. Number of Cases Filed in All Program Areas

Although the SEC's enforcement actions are up in most categories, there also are some notable declines. For example, the SEC brought 32 market-manipulation cases compared to 41 cases last year.[10] Though not attributable to any single cause, this decline may relate in part to a reallocation of resources. In September 2017, the Division announced the creation of the new Cyber Unit. Against the backdrop of the SEC's ongoing hiring freeze, the creation of the Cyber Unit drew from personnel in the pre-existing Market Abuse Unit, which housed much of the Division's "cyber"-related expertise.[11] In addition to cyber-related matters, the Market Abuse Unit historically has focused on complex cases involving insider trading, market manipulation, market structure issues and other large-scale or complex schemes in the securities markets. This shift in resources might account, in part, for the decline of market manipulation cases as well as other areas of focus for the Unit.

Speaking of the Cyber Unit, "cyber" cases formed very little of the Division's enforcement portfolio. SEC leadership described keeping pace with technological change as a core enforcement principle in last year's Report, and repeatedly noted this area as an emerging priority in public statements, with a particular emphasis on cryptocurrencies. Recently, Co-Director Avakian explained that, "[g]iven the potential of [initial coin offerings] to fundamentally alter the process by which issuers raise money, they have a significance to our markets that far outweighs strict notional dollar amounts." In its 2018 Annual Report, the Division argues that its "focus on cyber-related misconduct has steadily increased."[12] The Division reports that it brought twenty "cyber" cases this year; of these, "over a dozen" were cryptocurrency and ICO-related cases alleging violations of the anti-fraud and registration provisions of the securities laws, among others. Despite the attention they have received, these cyber-related matters made up only about 4% of 2018 cases. If and when the SEC's hiring freeze lifts, we anticipate the Division adding more staff in this area, and we would expect enforcement of such cases to increase in 2019.

The Division also claimed to "leverage its own technology to accomplish its enforcement goals."[13] That effort had at least one notable result. The SEC has effectively used data analysis to uncover alleged "cherry-picking" schemes by broker-dealers and investment advisers. Cherry-picking schemes involve financial professionals using hindsight and a lack of transparency to keep profitable trades for themselves, while allocating the unprofitable ones to their clients. In 2018, the agency brought nine such cherry-picking cases based on circumstantial evidence derived from sophisticated data analysis. The SEC's investment in data analysis has been cited in other kinds of cases, as well. For example, the SEC cited the Market Abuse Unit's Analysis and Detection Center for its assistance in investigating several insider-trading cases in 2018, including a high-profile enforcement action against former NFL player Mychal Kendricks. Given the SEC’s significant investment in this data analysis over the past five years, we expect more cases to result from this effort in the future.

In some of the smaller program areas, such as FCPA and public finance, the number of cases brought this year is consistent with 2017, though penalty amounts in these program areas appear to be declining overall. For example, although the SEC brought the same number of FCPA cases in 2018 as it did in 2017, total recoveries from these cases were noticeably lower. According to New York Times data tracking recoveries from cases filed in 2018, the SEC recovered $850 million in FCPA cases filed in 2017, but only $359 million in 2018 cases so far—the same number of cases, but with around half the recovery.[14]

Public finance cases, involving securities law violations by the issuers or dealers in municipal finance instruments, appear to have declined slightly, from 17 such cases in 2017 to 15 this year. This small decline is even less significant, however, considering that some of the 2017 municipal cases are better characterized as "spillover" from the SEC’s Municipalities Continuing Disclosure Cooperative Initiative, which mostly wrapped up in Fiscal Year 2016. Excluding those MCDC-type cases from the 2017 numbers, public-finance enforcement actually increased by one this year, suggesting that enforcement in this area remains consistent. And recoveries in this category increased substantially compared to last year, according to the New York Times data, reaching $5.9 million compared to just $1.3 million for 2017-filed cases.

C. Specialized Units

In order to assess the Division's allocation of internal resources, we analyzed not only the number and mix of cases in each program area, but also productivity across geographic offices and other enforcement units. In addition to relying on "generalist" enforcement personnel in its Headquarters and eleven regional offices that handle the full panoply of SEC cases, the Division also employs six specialized units to collect expertise on particular areas: the Asset Management Unit, the Complex Financial Instruments Unit, the Market Abuse Unit, the FCPA Unit, the Public Finance Abuse Unit, and the newly minted Cyber Unit. For years, the Division has used these groups to bring many of its headline-grabbing cases. But as this year’s results suggest, the Division's "Specialized Units"(with one important exception) bring a relatively modest proportion of the SEC’s enforcement actions. Assessing the progress and productivity of these units is extremely challenging. Although the "quality over quantity" adage is apt when evaluating the SEC's enforcement program as a whole, it is even more appropriate when assessing the Specialized Units, given the complexity of many of the cases they pursue. In addition, the Units also frequently offer expertise and personnel to other groups within the Division, making their contributions difficult to measure in simple terms. Nevertheless, when determining whether the Units are "right-sized" given the SEC's continuously declining resources, Division officers inevitably consider numerical production.

With those caveats in mind, our data show that the Specialized Units brought 87 cases (out of 490 standalone cases) in 2018; 32 of these were "investment adviser" cases brought by the Asset Management Unit, which, as discussed above, was arguably the greatest focus for the enforcement program this year. On the other hand, the Market Abuse Unit, which historically has handled some of the Division's most complex cases, has ceded some employees to the new cyber initiative, and brought only 18 cases—or about 4% of the standalone cases in 2018.[15]

And although the Division reported bringing a dozen "cryptocurrency"-related cases this fiscal year, just four of those (plus one market manipulation case and one insider trading case) as publicly attributed to its new Cyber Unit. Excluding the Asset Management Unit, the other five units combined are responsible for just over 10% of the SEC's 2018 standalone cases.

II. Penalties

As it did in 2017, the Division once again noted in its 2018 Report that cases with large disgorgement and penalty amounts make up a small percentage of its cases, but a significant proportion of the overall penalties ordered each year.

Last year's Report measured the Division's "largest" cases in two categories: those involving disgorgement over $100 million, and those involving penalties over $50 million. In 2016, the Division secured orders for disgorgement over $100 million in six cases (totaling $1.26 billion), and penalties over $50 million in four cases (totaling $706 million). Those totals declined in 2017, when the Division secured orders for disgorgement over $100 million in five cases (totaling $1.294 billion), and penalties over $50 million in just three cases (totaling $222 million). In 2018, the Division did not report this metric. Nevertheless, the number and magnitude of significant recoveries declined again: the Division secured disgorgement over $100 million and penalties over $50 million in just one case each—a $143 million FCPA and accounting settlement with Panasonic and a complex FCPA settlement with Petrobras involving about $85 million in penalties (net of credits).

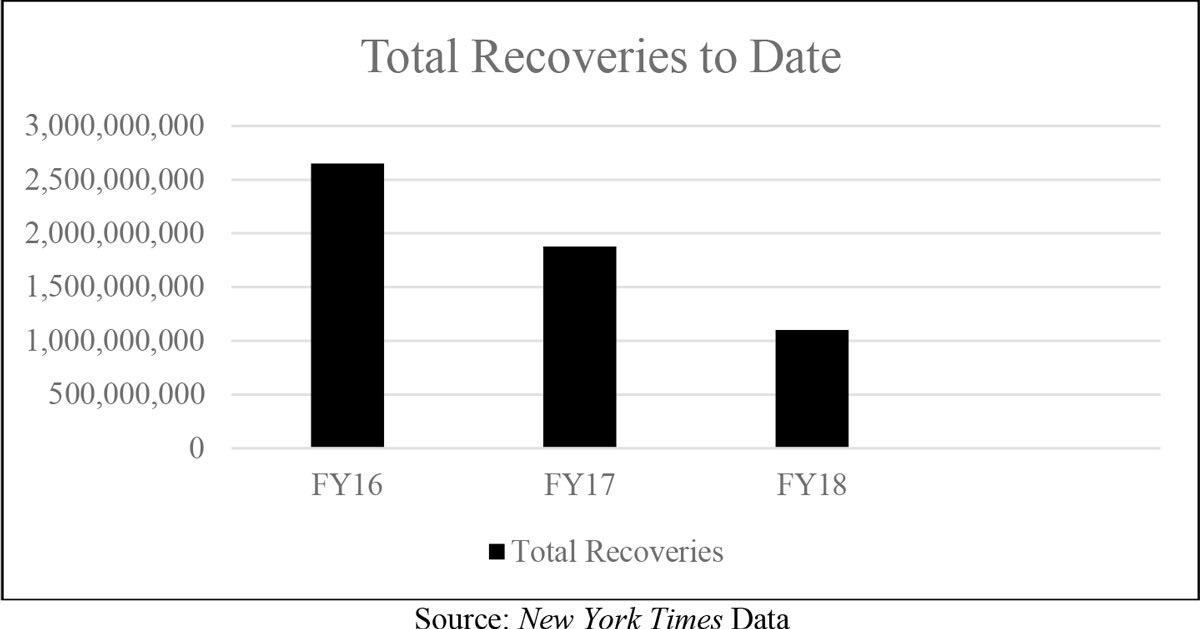

New York Times data on SEC enforcement activity confirm this decline in penalties. The Times data show that for cases filed in Fiscal Year 2018, the SEC recovered just over $1.1 billion in combined penalties and disgorgement. By contrast, for cases filed in Fiscal Year 2017, the Times data show that the Division recovered $1.898 billion, and for Fiscal Year 2016 cases, $2.649 billion. By this measure, 2018 represents a year-over-year decline in recoveries. The SEC itself, using a significantly different methodology for its calculations, reported that in 2018, the Division recovered $3.945 billion in combined penalties and disgorgement, compared to $3.789 in 2017 and $4.083 billion in 2016.[16] As the SEC also acknowledges, however, its 2018 results actually represent a decline in disgorgement from 2017, and its higher reported penalty amount is largely attributable to "a single case," from which the SEC is unlikely to recover the vast majority of its reported penalty.[17] Correcting for that outlier, from either vantage point, even as the overall number of enforcement actions appears to be consistent since last year, the magnitude of monetary recoveries has declined.

Though the Division argues that high-dollar settlements represent only one measure of enforcement success, market participants are sure to take notice of the decline in monetary remedies. Consistent with that decline, one of the case categories with increased activity last year—securities offerings—tends to involve matters that are smaller in scope and carry lower monetary remedies on average than more complex cases, such as those involving large financial institutions and issuer reporting.[18]

The Division also has recently emphasized its use of non-monetary remedies in enforcement settlements. Calling too great a focus on penalty numbers "counterproductive" in recent remarks, Co-Director Peikin pointed to several "case-specific" and "tailored" remedies, such as the settlement with Theranos founder Elizabeth Holmes requiring that she give up voting control of the company and ease the path for investors to recover money, and a settlement with Fyre Festival promoter Billy McFarland enjoining him from participating in the sale of securities. Although "conduct-based injunctions" have been around for a long time, the Division seems to be focused on expanding the use of this enforcement tool in new and creative ways. In its 2018 Report, the Division repeated that argument, highlighting some of the same cases and calling these special "undertakings" "[o]ne of the most effective forms of equitable relief in Commission enforcement actions."[19] Though an interesting counterpoint to single-minded focus on monetary recoveries, conduct-based injunctions are unlikely to become the primary method for judging the Division’s successes since their effectiveness is difficult to measure.

It also bears noting that the SEC’s arsenal of monetary remedies has recently come under fire. In June 2017, upending years of Enforcement Division practice, the Supreme Court held unanimously in Kokesh v. SEC that the SEC’s disgorgement remedy counts as a "penalty" under the applicable statute of limitations, meaning that in seeking disgorgement, the SEC is time-limited, just as it is with traditional penalties. The Kokesh decision is sure to impact the amount of disgorgement the SEC recovers each year going forward. The Division noted in its 2018 Annual Report that "the decision may cause us to forego up to approximately $900 million in disgorgement, of which a substantial amount likely could have been returned to retail investors."[20]

III. Individual Accountability

One of the Division's top priorities for 2018 was securing individual accountability for violations. Arguing in its 2017 Annual Report that "individual accountability more effectively deters wrongdoing" than pursuing misconduct by institutions, the Division explained that focusing on individuals "will send strong messages of both general and specific deterrence and strip wrongdoers of their ill-gotten gains." The 2017 Report noted that one or more individuals were charged in 73% of 2017's standalone actions.[21]

In 2018, the Division has maintained a steady pace of individual enforcement, charging individuals in 72% of this year’s cases.[22] According to our independent analysis, however, that rate is largely buoyed by two or three categories of cases that have a high proportion of individual defendants and respondents almost by necessity. Not surprisingly, 100% of insider-trading cases brought by the SEC in 2018 name individuals as defendants or respondents. Similarly, securities offering cases in 2018—including Ponzi schemes and pump-and-dump cases—name individuals as parties about 95% of the time.

However, in other areas, such as issuer accounting and disclosure and broker-dealer cases—where the ability to prove fraudulent intent by individuals is much harder—the number of individuals charged is lower. Issuer accounting, auditing, and disclosure cases name individual defendants or respondents in about 72% of 2018 cases. Only about 53% of broker-dealer cases involved individuals as parties and, not surprisingly, individuals were named in only 15% of FCPA cases this year.

More surprising is the number of investment adviser cases that include individuals as parties. Our data show that only about 56% of the 2018 cases involving investment advisers had individuals in the case caption. Given the frequency with which breaches of fiduciary duty arise in the investment adviser context, we were expecting the Commission to name more individuals in those cases.

IV. Conclusion

In our view, the Division acted on its stated plan to focus on "Main Street" retail investors, expanding the number of investment adviser and securities offering cases. At the same time, we note that there has been a decline in more complex accounting and market manipulation cases—which also impact retail investors—as well as in the amount of monetary recoveries generally.

In the year ahead, we expect the Division to continue its focus on harm to retail investors, and to expand its enforcement in high-technology cases, such as those involving cryptocurrencies, particularly as the Division expands its ranks by hiring additional investigators and subject-matter experts.

---

1. In the Division’s Annual Report, the SEC has divided the 2018 cases into twelve categories. Although we used the same categories, in approximately twenty cases, we concluded that the cases should be in different categories than those chosen by the Division. As a result, although we report the SEC’s categorizations in the charts below, our statistics relating to the various categories are slightly different than those offered by the Division in its Annual Report. In some instances, the cases involved conduct that touched on more than one category. In a handful of cases, we chose one of the appropriate categories and the Division chose another. In other instances, the conduct fell within one category but the defendants/respondents appropriately fit in a different category that corresponded with a class of regulated entities. In a third set of cases, we simply disagreed with the category chosen by the Division.

2. 2018 Annual Report, U.S. Securities and Exchange Commission, Division of Enforcement (“2018 Annual Report”) at 1.

3. 2018 Annual Report at 4; id. at 14.

4. 2018 Annual Report at 14 (noting the greater propensity of individuals to litigate).

5. 2018 Annual Report at 14.

6. 2018 Annual Report at 2.

7. Agency Financial Report, Securities and Exchange Commission, Fiscal Year 2017 at 42.

8. 2018 Annual Report at 8.

9. The New York Times data tallies payments based on the year in which the SEC's case was filed. Thus, to the extent that remedies were ordered this year in a case filed in Fiscal Year 2017, they would count toward the Fiscal Year 2017 total.

10. Market manipulation refers to frauds involving trading activity that interfered with the free and fair operation of a securities market.

11. 2017 Annual Report at 2.

12. 2018 Annual Report at 7.

13. 2018 Annual Report at 3.

14. In contrast to the SEC's own penalty-calculation methodology, the Times data do not credit the SEC as recovering money when, though the SEC orders a payment, the money actually is paid to the Department of Justice or a foreign government.

15. The most significant of these included settlements with Merrill Lynch in a broker-dealer-related case resulting in a $42 million penalty. See SEC Release No. 33-10507.

16. It is logical that the SEC's calculations would be higher than the Times's, because whereas the SEC appears to report all recoveries in 2017, regardless of when the case was initially filed, the Times totals the recoveries only from cases filed in that year. Thus, the SEC is reporting recoveries in 2017 from cases filed in prior years as well. And, as more 2018-filed cases are resolved in the future, the Times's 2018 recovery total will grow.

17. 2018 Annual Report at 11 & n.17. The Division is referring to its Petrobras FCPA settlement, which, through a complex settlement methodology, involves penalties and disgorgement of approximately $1.8 billion, but which, as noted, net of various credits for sums paid in parallel proceedings, appears likely to result in payments to the SEC of only about $85 million. The Times's data only credits the SEC for this net penalty amount.

18. Nevertheless, even as issuer reporting cases are down overall, one notable subset of those cases has been consistent year-over-year: the number of Fortune 500 companies they target. We identified three such cases in 2016, and five each in 2017 and 2018.

19. 2018 Annual Report at 12.

20. 2018 Annual Report at 5; id. at 12.

21. 2017 Annual Report at 11.

22. 2018 Annual Report at 12.

Back

Back